Making cents for Northland farms with the ETS

John-Paul Praat and Bob Thomson, New Zealand Tree Grower May 2011.

The ETS imposes increased costs on everyone and of course no one thinks that is fair, farmers included. However, the ETS presents some farmers with opportunities to make money. The potential effect of the ETS on two Northland properties has produced interesting results.

Balancing deficits

Between 1990 and 2008 New Zealand’s emissions increased by 23 per cent. Since 1990 this responsibility has largely been taken care of by new forest plantings which absorb and store atmospheric carbon dioxide. Additional planting will be required to balance expected deficits as those forests are harvested and replanted. Under the ETS, the energy and industrial sectors are currently required to purchase carbon credits to offset half their emissions, a level which will increase in 2013. This requirement creates the market for carbon credits in New Zealand.

Agriculture will also be required to purchase carbon credits from 2015, although initially to offset only 10 per cent of total livestock emissions. Meat and milk processors will purchase carbon credits on behalf of farmers and will probably pass the cost on as a levy on produce.

Forestry generates carbon credits which can be entered into the ETS and used to offset emissions, or traded for cash. Carbon credits have been available annually since 2008 for forests planted after 1990 on land not previously in forest.

Greenhouse gas emissions from agriculture

Livestock grazing on pasture emit greenhouse gases, mostly in the form of methane emitted from the rumen and nitrous oxide from activity in soils under pasture. The total annual greenhouse gas emissions from a farm can be calculated as carbon dioxide equivalents, using internationally agreed protocols. A New Zealand Unit (NZU), the standard measure used for carbon accounting, is equivalent to a tonne of carbon dioxide.

New legislation has been passed since this article was first prepared which specifies the way animal emissions will be calculated. Emissions will be calculated from an average value for New Zealand conditions per unit of production such as the number of head slaughtered and kilogram of meat produced. The calculations are based on national averages.

Agricultural emissions have been recalculated based on the production from the farms discussed here and are not materially different from the quantities shown.

Pohoatua

| Greenhouse gas source annual emissions |

Tonnes carbon dioxide NZUs |

|

|---|---|---|

| Petrol | 4,300 litres | 10 |

| Diesel | 270 litres | 1 |

| Electricity | 6,183 kWh | 1 |

| Nitrogen | 9.2 tonnes | 45 |

| Sheep | 1,466 | 484 |

| Cattle | 580 | 992 |

| Total | 1,540 | |

Pohoatua is a traditional sheep and beef operation with around 4,500 stock units, situated about 25 km west of Whangarei. The farm has an effective grazing area of 360 hectares with a mixture of flats and rolling country.

The farm’s production base is 850 ewes and 620 cattle. The ETS will initially result in some cost increases to farmers as suppliers of diesel, electricity, fertiliser pass on their own carbon liability costs. At first the farmers’ liability for livestock emissions will be limited to 10 per cent. At $25 a unit this will amount to a levy in 2015 for Pohoatua of about three cents per kilogram of beef and six cents per kilogram of sheep meat.

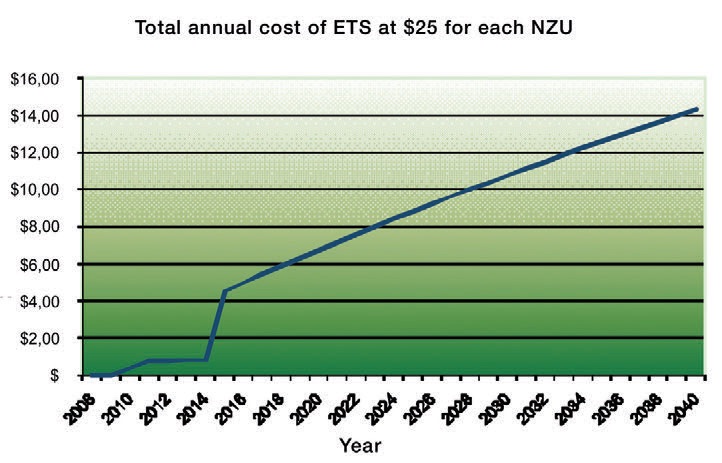

In 2011 the annual cost at the farm gate will be $802. However in 2015 the cost will be $4,553 and by 2040 the cost could be $14,336, depending on the carbon price at that time.

Potential forestry credits

There is little that can be done to reduce livestock emissions immediately without reducing stock numbers, so we have assumed emissions remain constant in the short term. Changes in the carbon price will have a direct effect on the final costs of any scheme. Carbon credits can be claimed for forests planted after 1989 on land not previously forested. Access to these credits reduces a farm’s exposure to future increases in the carbon price, significantly reducing business risk, and helping to build a resilient farm. Because Pohoatua lacks suitable existing forest, and the farmer wants to address the carbon imbalance, we suggest a forestry regime to generate carbon credits sufficient to offset emission liabilities for the next 30 years.

A cubic metre of stem wood from a radiata pine tree is approximately equivalent to a tonne of carbon dioxide, which equals an NZU. A pine tree can accumulate about 2.5 tonnes of carbon dioxide in 30 years.

Forest management

The rate of carbon accumulation or sequestration varies with species, climate, age and management regime. The standardised ‘look-up’ tables describe accumulated carbon based on species, age and region. These are used to calculate carbon credits accumulated during a forest’s life, as well as liabilities at harvest time. Manipulating these aspects can have a significant effect on the value of forestry carbon credits to a farm business.

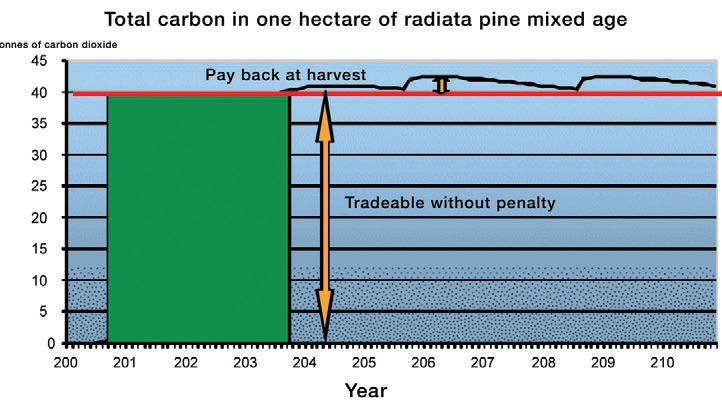

Small woodlots, usually established all at once using a single species, result in an even-aged stand which can be managed for timber in the most efficient manner. However this even-aged regime limits opportunities for carbon forest management. Under the current ETS rules, timber removed at harvest creates a carbon deficit and must be paid back.

The black line in the diagram represents accumulated carbon within an even-aged stand. At harvest the carbon in logs is removed but some remains on site − stumps, branches and roots slowly break down and are replaced by the new growing forest. This is why the black line does not drop back to zero at harvest. In the example shown, the first crop retains around 185 tonnes of carbon dioxide equivalent per hectare, which would remain tradable without the requirement to pay it back at the time of harvest. This base quantity of stored carbon is a one-off and once claimed and sold, cannot be sold again.

A way to store more carbon for trading and to reduce the requirement to repay carbon credits at harvest is to establish a new forest, or manipulate an existing forest, into a mixed-aged stand. There are various ways to achieve a mixed-aged forest. In the theoretical example shown in the graph below one hectare is planted every year for 30 years. Each year after the 30th year, one hectare is harvested and replanted.

As the graph shows, the forest owner will be able to sell 400 carbon credits per hectare without having to repay any of those at harvest. These credits are effectively a permanent carbon sink.

Carbon trading and area required

Assuming a conservative approach to carbon trading is desirable, then only that portion of forest carbon which is safe to trade without incurring a harvest penalty should be sold to offset farm emissions liabilities. To safely offset these liabilities, an even-aged forest would need to be more than twice the size of a mixed-age forest.

| Carbon price | Total cost to 2040 | |

|---|---|---|

| No forestry | With 26 hectares of forestry | |

| $25 | $255,525 | Cost of forest $60,000 |

| $50 | $511,050 | Cost of forest $60,000 |

| Current | Less 26 hectares | Difference | |

|---|---|---|---|

| Revenue − sales less purchases | $271,410 | $257,657 | -$13,754 |

| Expenditure | $66,517 | $63,755 | -$2762 |

| Gross margin | $204,894 | $193,902 | -$10,992 |

| Gross margin per hectare | $569 | $581 | +$11 |

Total emissions liabilities for Pohoatua between 2010 and 2040 will be 10,327 NZUs. We calculate that, at 400 NZUs per hectare, 26 hectares of new mixed age forest would offset this amount.

Computer modelling was used to assess the effect on the livestock operation of converting 26 hectares of grazing land to forestry. Several paddocks estimated to be producing pasture at only 70 per cent of the farm’s average rate per hectare were identified for planting in trees.

On the face of it, the forestry would save an average of $8,500 a year but would cost the farm $10,992 in reduced gross margin. Therefore the investment in forestry does not stack up at current prices but we calculate that the investment would break even at $32 a unit.

To achieve a mixed-age forest, we suggest that planting should be staggered so that five to six hectares is planted every five years. If the harvest age varied between 25 and 35 years of age, this would potentially yield an average return from timber of around $20,000 a hectare each year, which would compensate for the lost gross margin from livestock.

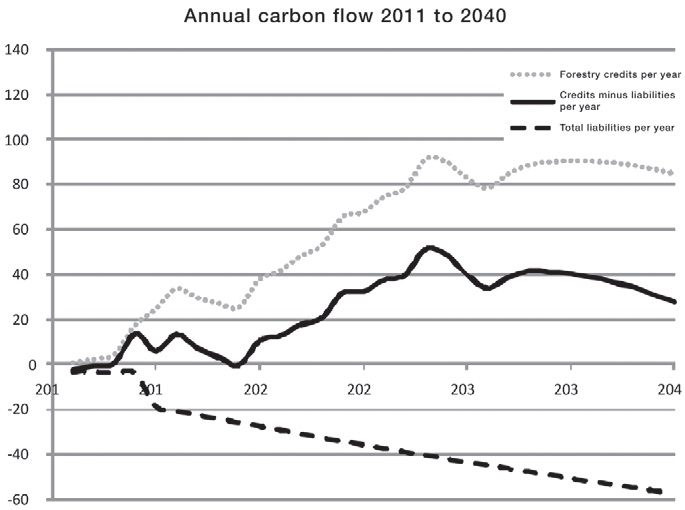

The next graph shows the balance between farm emission liabilities and forestry credits for such a staggered planting of radiata pine. This regime would generate sufficient carbon credits to offset farm emission liabilities, provided that the balance of credits minus liabilities remains above zero. This staggered approach would allow a farmer to start integrating forestry into the business, reducing the risk of future increases in the price of carbon.

After 30 years, once the mixed-age forest enters the phase of periodic harvest and replanting, a new area of forest will be required to sequester further emissions. Alternatively, rotation length could be extended to increase the quantity of carbon permanently stored. This might occur in cases where the price of carbon is high and the price of timber is low.

Millbrook Station

The other farm we assessed was Millbrook Station, a sheep and beef farm. The effective grazing area is 478 hectares and the current livestock base is 628 ewes and 702 cattle. Total annual greenhouse gas emissions from Millbrook Station are 1,401 NZUs. Livestock are the source of 97 per cent of emissions. The total annual cost of the ETS to Millbrook Station was calculated to be $557 in 2011, $4,259 in 2015 and $12,951 in 2040.

Existing forestry

Millbrook Station is eligible to claim carbon credits under the ETS for existing forest established after 1989 on non-previously forested land. This existing forest comprises 20 hectares of radiata pine planted in 1995. In addition, the farm can claim credits for 166 hectares which has been retired to native forest reversion.

In 1990 that land was being grazed by goats and sheep and had some gorse but no significant forest. Critically, less than 30 per cent of the area was covered with forest species and the prevailing grazing management would have prevented it reverting to forest. Had there been 30 per cent or more cover of forest species including manuka or kanuka, the land would have been classed as forest and would not be eligible for carbon credits under the ETS.

Calculating the carbon credits

At present, carbon credits can be claimed for carbon accumulated from January 2008 onwards. Annual credits of three tonnes per hectare per year are used here to calculate accumulation by native reversion. Revised values recently released by MAF are double that.

Using the look-up tables, we calculate that the forest areas on the station are currently accumulating approximately 1,268 NZUs a year. When agriculture first enters the ETS in 2015 it must meet 10 per cent of its emissions, which for Millbrook will amount to 140 NZUs. This will be more than offset by its annual credits from forestry and native reversion. Over the period between 2008 and 2015 Millbrook will potentially be able to claim a surplus of 8,666 NZUs.

Matching land use

| Land type | Annual production average kilograms dry matter per hectare |

|---|---|

| Flat/easy land | 12,950 |

| Rolling hills | 8,776 |

| Steep hills | 4,947 |

A wide range of land types occur within the 1,087 hectares of Millbrook Station. A land use capability survey detailed the productivity of the land resource. Five distinct land management units were identified. Results for three broad land type categories are shown in the table below. The flat and easy land had annual production of almost three times that of the steep hills. This low-productivity steep land was also receiving gorse spraying every three years at a cost of $600 a hectare. The combination of low productivity and high cost resulted in a negative gross margin on this land type. From this land use analysis, 100 hectares of the steeper land was identified for establishment of new forest, the proposal being to plant a range of species including radiata pine, poplar, eucalyptus, Japanese cedar and redwood.

Proposed new forest and farm productivity

An assessment was made to determine the effect on the livestock operation’s productivity and profitability of converting 100 hectares of steep grazing land to forest. The analysis showed that gross margin for the farm would be reduced by only $17,939 or 8.5 per cent. Offsetting this small decline in farm income would require a very modest increase in return of $47.50 per hectare per year across the remainder of the farm.

| Current | Less 100 hectares of steep hills |

Difference | |

|---|---|---|---|

| Revenue | $298,897 | $269,367 | -$29,530 |

| Expenditure | $86,809 | $75,218 | -$11,597 |

| Gross margin | $212,088 | $194,150 | -$17,939 |

| Gross margin per hectare | $444 | $514 | $70 |

In addition the cost of maintaining the steep land in pasture exceeded the return and an average of $20,000 a year could be saved on gorse control. It is also expected that a further $20,000 could be added to farm income by diverting the work on the 100 hectares to the more productive areas of the farm. The analysis showed that focusing livestock production on the better land and producing timber and carbon on less productive land will improve overall profits, probably reduce work requirements, and improve overall farm efficiency.

Funding the new forest

Assuming the entire 100 hectares is planted in 2011, it is possible to accumulate 23,893 NZUs during the first 10 years. At a current market value of $20 a unit this equates to a gross return of $480 per hectare per year, similar to current returns from livestock. If the average establishment cost is $2,000 a hectare and the NZU price $20, Millbrook Station will have sufficient surplus carbon credits to sell from existing forestry to fund the proposed new forest over the next six years. There will also be sufficient credits available to address the expected harvest liabilities from the 20 hectares of existing pine in 2025.

Millbrook Station is ideally placed to capitalise on the potential returns from carbon while minimising the risks. Establishing the new forest could be done over several years and funded directly from carbon sales so that no extra capital would be required.

Conclusion

The contrasting potential effect of the ETS on these two farms shows that detailed analysis of land productivity and profitability is vital in making the best land management decisions. On the basis of this work we suggest a rule of thumb could be that for areas of pasture producing less than 50 per cent per hectare of the farm’s average rate, afforestation should be seriously considered. The Millbrook Station example shows how farms with existing post-1989 forestry have ideal, low risk opportunities to achieve this.

In a wider sense, access to carbon credits insulates a farm business from the potential cost of liabilities from livestock emissions by neutralising carbon price effects over the medium term of 30 to 50 years. During this time technological solutions to livestock emissions could be developed and implemented. It could be especially valuable if future carbon prices are high. Forestry provides multiple benefits and forms part of a sustainable land management strategy with positive environmental and economic results. Farming operations which already include forestry planted after 1989 are not only more resilient to droughts and floods but will be ideally placed to address any increase in costs imposed by the ETS.

An earlier version of this article was first published in the journal Primary Industry Management. John-Paul Praat works for PA Handford and Associates and Bob Thomson for AgFirst Northland.